“Are we doing anything with bitcoin?”

You’ve probably heard that question from a board member. When they ask, maybe you say something noncontroversial like “We’re looking into it.” Or maybe you change the subject: “How about those Mets? Injuries are killin’ ’em this year.” You can’t come out and say what you’re really feeling: “Look at bitcoin with your real eyes, not your crazy eyes!”

But seriously, anyone with a risk management background should be a cryptocurrency skeptic. Here are five reasons why.

1. Volatility

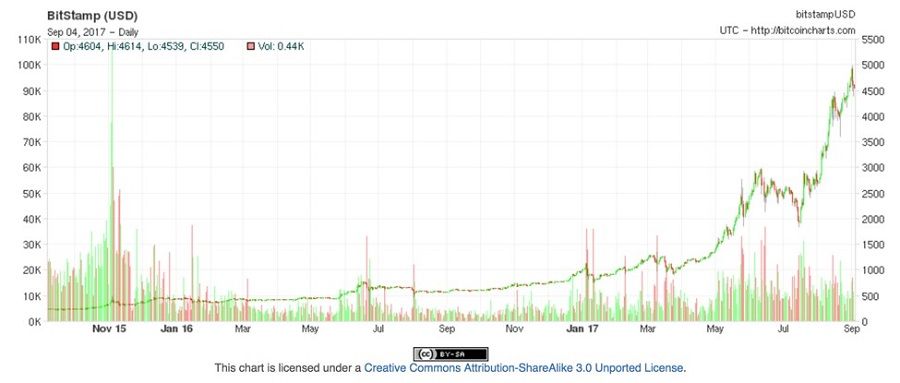

The recent rocket-like rise of the conversion value of bitcoin to $4,000 will have even more board members (or directors or bartenders or barbers) asking you the same question in the months to come. But has everyone forgotten that just three years ago, bitcoin was the worst-performing currency in the world, losing 56 percent of its value?1

The meteoric rise in the value of bitcoin comes from the perception that the bitcoin community has solved the years-long “block size” problem, which had led many to claim bitcoin was a failed experiment.2 The main bitcoin fork introduced Segregated Witness (SegWit),3 which allows offline transaction chains. A new fork of bitcoin introduced in August 2017, called Bitcoin Cash,4 also increased the blockchain block size. Both of these improvements should speed up transaction verifications (though it would be nice if they were the same fork. Thanks, guys!).

Speculators are now resuming their irrational exuberance.

Sure, volatility is an aspect of currency; In Real Life (IRL), arbitrage markets exist to absorb that risk. And you’re not dabbling with them, are you?

2. Maturity

There are thousands of ways to steal real money IRL; fraud, impersonation, counterfeit, embezzlement, and money laundering are just the big ones. If there exists a way to steal money, someone, somewhere has tried it, and maybe even given it a name, like pig in a poke,5 the fiddle game,6 or the one-eyed glim-dropper.7

IRL, we have infrastructure to deal with these schemes. Laws, for one. And courts, insurance, Federal Deposit Insurance Corporation (FDIC), double-entry accounting, and regulation. What does cryptocurrency have? Not much. Just some blockchain stuff running on volunteer computers. Sure, the blockchain verification sounds like built-in accounting, but if you can be anonymous, what exactly is the point of all that accounting? What is the point of cryptographically proving that someone stole your bitcoin and spent it on a Samsung TV, but you have no idea who it was?

In Pennsylvania this summer,8 a man admitted to stealing $40 million worth of bitcoins. The authorities didn’t charge him with theft, because while bitcoin is money, it isn’t legal tender.9 Also, he was going to get a fake passport with Jeremy Renner’s picture on it, LOL. It’s so easy to steal bitcoin; even this guy can do it.

Image by Eva Rinaldi / License Creative Commons

3. The Nation State

One of the supposed benefits of bitcoin and other cryptocurrencies is that they aren’t tied to any particular nation state. This prevents bitcoin assets from being frozen by the state, and gives consumers the freedom to do anything they want with their money.10

State sponsorship of a currency has obvious benefits, though. Consider:

In the 1990s, George Soros nearly single-handedly destroyed the pound sterling by betting that it was overvalued.11 To keep the pound from a precipitous fall, the UK government had to raise the interest rate to 15 percent. Pledging the resources of 80 million Britons kept the pound afloat. Had the defense failed, however, the pound would have fallen against all other currencies, possibly leading to a nationwide depression.

Who’s going to defend cryptocurrency from the next Soros?

And consider this—in the United States, the Secret Service has only two jobs:12 protecting the president, and protecting the currency (mostly against counterfeiting).

Where is the Secret Service for cryptocurrency?

4. All Those Flipping Thefts

For a currency that was designed to make theft impossible, bitcoin has a terrible and ironic history of constant, massive thefts. You can read the entertaining Blockchain Graveyard13 list of 44(!) cryptocurrency bank failures, most of which were due to theft. Mt. Gox, the world’s largest repository of bitcoins, failed after 744,000 bitcoins (representing 6 percent of the worldwide total) were stolen. Today’s market value of those bitcoins is $3 billion. They are still out there somewhere, and they haven’t been used. One of the benefits of distributed ledgers is that everyone will know as soon as someone tries to use one of them.

IRL, banks fail all the time.14 Occasionally it is due to mismanagement, but often it’s just market forces at work. The FDIC in the United States guarantees the first $100,000 in deposits for each customer in any failed bank, and then ensures the easy transition of assets as the failed bank is folded into another bank. After 4,000 years of banking,15 ;the financial community still hasn’t figured out how to avoid bank failure—but at least there’s a process for cleaning it up. Cryptocurrency banks appear to fail all the time16 as well, but there is no depositor guarantee. The associated monies just vanish.

If, IRL, bank failures are inevitable, why would anyone think that it would be different for cryptocurrencies?

5. Quantum Expiration

Bitcoin and most other cryptocurrencies seem like the bleeding edge of cryptographic technology, but they are actually heavily dependent on asymmetric encryption algorithms that are decades old. And those underlying algorithms are not resistant to quantum computing, should a quantum computer ever be built. Bitcoin private keys are just 256-bit Elliptic Curve Digital Signature Algorithm (ECDSA) keys, so a quantum computer with just a few thousand qubits could, in theory, find every wallet’s private key in the bitcoin universe. Won’t that be a fun day!

Infrastructure Isn’t Just Technology

The financial community has the largest cybersecurity budgets in the world. And even with regulation, nation-state support, security teams, threat intelligence, and every security inspection device imaginable, they are just barely capable of keeping hackers from stealing all the monies. The CISOs for those companies know that they need more, way more, than just technology to secure a bank.

If you think all you need is technology to defend against bad guys, you shouldn’t be a CISO. But that’s all cryptocurrency is: technology.

Does the underlying blockchain technology have a place? Maybe. Distributed cryptographic ledgers are pretty cool, after all. And people are talking about using it for identity and access management for IoT. Yeah, that smells like a solution in search of a problem, but you could assert IoT as an answer to our vexing question, “Are we doing anything with blockchain?”